Every three months, I post my net worth on this site. This has proven to be a hotly anticipated post by readers. While I considered squashing it at two years, the outcry from readers was loud enough to encourage me to keep posting these numbers publicly.

There are a few major reasons for these updates. First, I want to dispel the myth that money is a taboo topic that we should not openly discuss. This is important in my role as an educator of future medical professionals. Second, posting net worth updates holds my family and me accountable. Third, it proves that you, too, can make financial mistakes and still obtain your financial goals.

My mistakes have included forbearing on my student loan debt during training (If your Debt to Income Ratio is <1 click here to get a cashback bonus by refinancing here), getting hosed by an insurance agent, and many more. Then, I became a DIY investor and started crushing it. And you can, too.

Each update starts with a summary of the previous updates and then we dive into our assets and debts as they currently stand. Finally, the newest updated networth is posted at the end.

A Quick Update on The Last Two Years

This is the next installment of the Physician Philosopher Net Worth updates. To read my previous Net Worth Updates click the following links.

- This post discusses some of my numbers and goals when I first started this site in November 2017.

- Here is my first quarterly net worth update written six months after I started my job as an attending (numbers from January 2018)

- Second Quarterly Net Worth Update (4/27/18)

- The One Year Out from training Quarterly Net Worth Update (7/30/2018)

- 15 Months Out from training (10/2018)

- 18 Months from finishing fellowship (1/2019)

- 21 Months Out (4/2019)

- Two Years Out from training (07/2019)

- 27 Months after finishing fellowship (10/2019)

- Our net worth at 30 months out can be found here (1/2020)

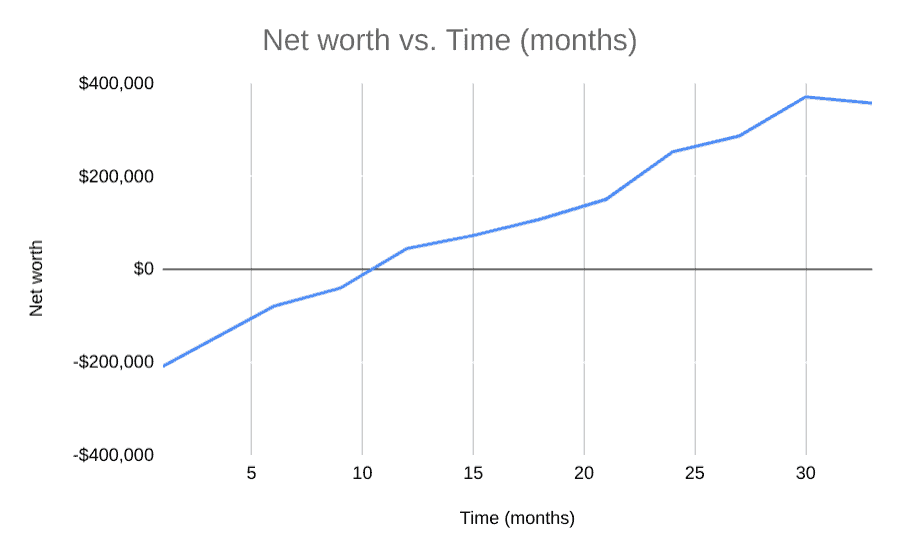

The Last Two Years in Numbers and Pictures

If you don’t feel like clicking through those, our net worth started at negative (-) $208,000. This is how our net worth has changed at each of those time points:

- Six months out, it had improved to (-) $78,819.

- By 9 months out we were at (-) $40,270.

- We finally had a positive net worth one year out at +$45,000.

- At 15 months, we had reached $73,000.

- It took us 18 months to get to a six figure net worth: $107,718.

- After 21 months, we were sitting at a net worth of $150,820.

- With the 24 month update, we shot up to $252,974.

- At 27 months, our net worth was $287,155.

- 30 Months out, we were continuing strong at $371,058.

- And finally, the drop came that we all knew would come…

In graphical form, it looked like this for the past three years.

I normally don’t include the current net worth until the bottom, but I wanted everyone to see the dip we took in our net worth over the last quarter in graphical form. It is a bit depressing to see it go down, but that’s what happens when the market takes a 30% nose dive and you are heavy in stocks.

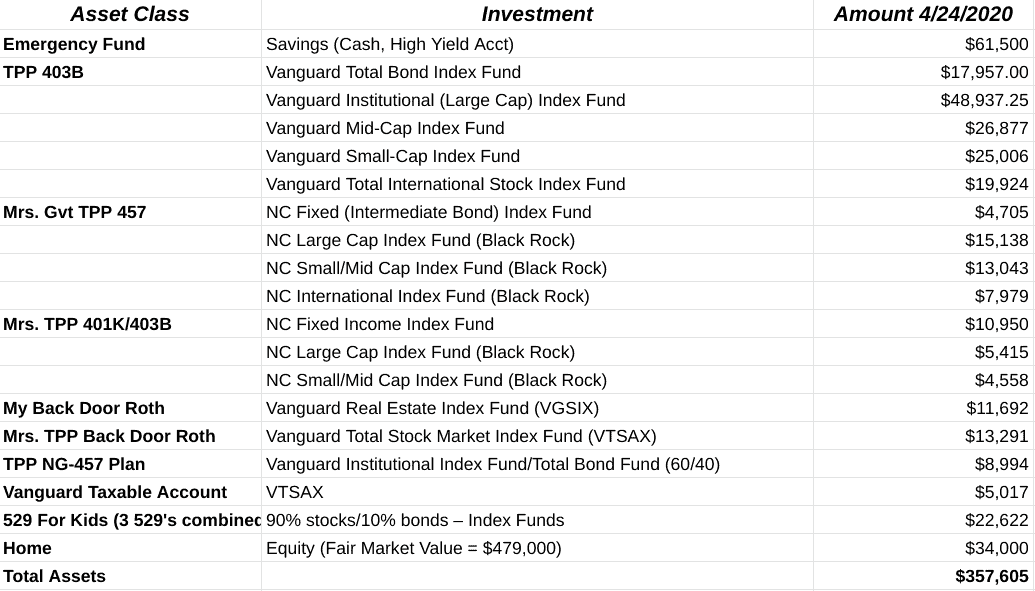

33 Months After Fellowship: Assets

Since the release of my book (click the link to head to Amazon where you can purchase it), I have been non-anonymous on this site. I have always found that transparency is helpful.

Here are our assets and the dollar amount for each category. All of this is as of 4/24/2020.

Comments on Our Assets

Our Annual Savings Goal

Our annual investment goal remains between $115,000 and $125,000 with a goal of having around $3.0 million in assets by the time we are 45. This doesn’t include any “passive income” we have coming in through The Physician Philosopher or the Money Meets Medicine podcast.

We get to this annual savings number by investing in the following accounts:

- $45,000 in my 403B

- $12,000 in my non-governmental 457 (though I may increas this to $19,500 given our increasing cash flow)

- $19,500 in Kristen’s governmental 457

- $19,500 in Kristen’s 403B/401K (we will max this out in 2020 for the first time)

- $12,000 in our Backdoor Roth IRA (here is a tutorial for your first Backdoor Roth IRA, if you need it)

- $3,000 required pension for Kristen

- $7,100 Health Savings Account (we decided to cash flow our medical expenses and save these valuable dollars)

- $6,000 in a brokerage account

Adding this together amounts to $124,100, which is within our target annual savings rate. All of this is automated out of our paycheck each month outside of the backdoor Roth IRA, which happens in a single transaction in July when I receive my annual bonus.

If you add in the $1,250 we put into our kid’s 529 plans each month, our total annual savings is actually $139,100. With our current assets, and assuming a conservative 6% average annual growth in the market, we should crack $1 million in assets by age 37, and we will reach $2.5 million by age 43.

Don’t know how to perform a Backdoor Roth IRA – Click here for a step-by-step Backdoor Roth IRA tutorial at Vanguard.

Debts: 30 Months Out

Here are my family’s current debts.

| Class | Amount of Debt |

| Home Mortgage (~$445,013) | |

| Total Debt (excluding mortgage) | $0 |

Some Comments on Our Debt and Spending

Being debt-free outside of our mortgage has been simply amazing. I don’t regret for a second paying down debt that could have been leveraged into the market.

Our mortgage is next. Now that we are automatically meeting our annual savings goal, any additional money we make will be going towards the mortgage per The 10% Rule (update: it is a 25% rule now).

In fact, we are in the process of refinancing our home to a 15-1 Adjustable Rate Mortgage (ARM) at 3%. Despite the low-interest rate, we still plan to pound money into our mortgage to have it paid off over the next 5 to 7 years.

Want the step-by-step process we used to crush these goals? Click here to join the Medical Degree to Financially Free wait list. The next course launches for students on June 15th.

Net Worth

Net Worth = Assets – Debts

$357,605 – $0 = $357,605

**For the purest out there, if we were to include the house in our debt, we would also include the full value on the home on the assets side. This would result in the same net worth.

Welp, it finally happened. Our net worth took a hit because it is almost entirely dependent on our assets at this point. So, when the market turned into a bear, so did our net worth.

Not to worry, though, good investors play the long-game and I know that being heavy in equities will pay off later! Remember to always stay the course. That is what we are doing, and will continue to do.

- Our net worth dropped by $13,453 in the last quarter. This is despite investing $10,592 per month automatically out of our paycheck (or $31,775 per quarter). That shows how impressive this drop was!

- Since I finished training (when our net worth was -$208,000), we remain up $565,605 despite the big loss we took.

- We are still on pace to become millionaires by age 36 or 37. Our FI number should get be accomplished at age 43-45.

- We no longer “live on half” as Physician on FIRE prescribes. That said, we are still putting away around 30% of our gross base salaries. With our debt outside of the mortgage gone, we will probably do the same with any bonus money or side hustle money from this blog.

This should serve as proof that living like a resident after training works if you make a plan and stick with it!

Take Home

Don’t let the big hungry bear market scare you into bad financial decisions. The further along the journey you are, the more a drop in the market will impact your situation. Don’t fret! Stay the course. It’s all going to be okay.

Going forward, our goal will be to find contentment in our current life. We are now in the steady stages of wealth accumulation. Though this is automatic, our focus is on the path to financial independence. We want to enjoy this journey along the way through Partial FIRE.

That’s our story. What’s yours? How did the market drop impact your net worth and investments? Leave a comment below.

The pandemic certainly put an end to the incredible bull run we had.

My net worth also dropped during the quarter but due to a strong April rally (and rebalancing to take advantage of the dips in some asset classes) on April 30 I hit a new personal net worth high (just topping out my net worth in February before the craziness happened).

Why do you not include the blog and/or partnership with WCI as an asset?

Good question. I am not sure I have a satisfactory answer.

The main reason is that the “value” of that is highly variable depending on how you value the business. In addition, I cannot share contractual details about the set up.

Suffice it to say, that the money that is “mine” from my business account is included in the numbers above. So, if is included to some extent, but not in granular details

Does your employer offer Vanguard funds in your 403b? If not, how do you go about investing in them in your 403b while still maintaining your employer match?

Hi! I find your numbers incredibly useful because we hover (I suspect) around the same savings levels. I would love an estimate of your monthly expenditures. Doesn’t have to be super granular, but on average, what is your spending each month?

We are also going for about $120K/yr savings goal plus 529s. (I do struggle with how much to put in those!). Anyway, a rough estimate of your annual spending would be really helpful!

Hmmm… That is probably worth a deep dive. I’ll write a post on that. We don’t focus on it anymore as we always have money left over even after accomplishing these goals… But I’ll look into it!

Strong work, TPP! Any reason you replicate the portfolio across your main employer accounts? You could simplify with an asset allocation across your entire portfolio.

I just use the options available to us in the accounts. I wish we had a total stock market fund in either retirement account, but we don’t.

I am definitely in the camp of focusing on overall asset allocation for the entire portfolio, though.

Maybe it’s listed in previous posts but I’m curious as to what your income is.

Last year our gross income was around $500,000. Saved >130k and paid off car debt last year. About 50% of our income went toward building wealth. Probably closer to 30-40% now.

Strong work and great commitment!

How are you able to save 45k in 403b? Isn’t annual cap 19.5k? (sorry if I missed the breakdown in an earlier post but I couldn’t find it)

Hey Jay,

Good Question. The max that can be placed in a 401K or 403B is $57,000 annually. This has two components. The first is what you are referencing- the employee portion, which has a maximum that YOU can place into it of $19,500. The second is the employER portion, where your employer can either match or contribute up to the $57,000 annual limit for 2020.

My employer matches/contributes a lot, but not the full amount and it usually ends up being around $45,000 total (my $19,500 plus what my employer contributes).

Jimmy / TPP

Thanks Jim for that clarification! and that’s awesome! I am in academic medicine too and my employer matches no where near that amount. That’s fantastic.