Last year was the first year that my employer offered an Health Savings Account (HSA). In the personal finance world, the stealth wealth IRA feels a bit like an echo chamber, though. It seems that everyone out there recommends using an HSA without a second thought. Today, I want to discuss the basics behind an HSA, and then walk you through my thought process as my family and I decided whether to use an HSA or not. Let’s hit some high-yield questions and sort it all out.

And, if you are brave it out all the way til the end, I’ll discuss how to determine if you should use your HSA for big expenses as they are incurred. I hope that this post serves

How does an HSA work?

In order to have access to an HSA, you have to have a High Deductible Health Plan (HDHP). For that information, skip to the next section.

Assuming you have access to an HSA, how does it work and what’s the big deal? Some have called the HSA the Stealth IRA. The reason for this is because of how the HSA works.

When you put money into an HSA, it is pre-tax money. It will then grow tax-free (including the gains). And, if taken out for health care costs, the money will never be taxed. For this reason, it is the only triple tax free savings option that exists.

Once this pre-tax money is in place, it can then be invested once you pass a certain threshold. At my HSA custodian (HSA bank), you must have a balance of at least $1,000 to invest the money. However, once you reach this number, you can place the HSA money into index funds, just like you would in your 401K, 457 plan (if you use it), or your backdooor Roth IRA.

What if you decide to take the money out for non-health care related expenses? If you do that before the age of 65 you will incur a fine. The non-qualified withdrawal fine is 20%, which is an absolutely massive fine. However, you can use the HSA money tax-free at any point if you have a qualifying expense (more on that below). For example, we put $7,000 into our HSA for the 2019 tax year, but ended up using about $3,000 of that when I got diagnosed with Grave’s disease. That money never got taxed or fined despite being younger than age 65, because it was a qualified expense.

Once you reach age 65, things change for the better.

After 65, you can take money out of your HSA penalty free for any reason (qualified or non-qualified) without the 20% penalty. This is why some call it the Stealth IRA. It becomes another pre-tax tax advantaged account, just like a 401K or 403B.

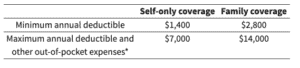

What is a High Deductible Health Plan (HDHP)?

In order to have access to an HSA, you must have a High Deductible Health Plan (HDHP), which is defined by the IRS as having the following deductibles and out of pocket expenses:

As you can see, not everyone will meet this requirement. However, this is necessary in order to take part in an HSA.

What can I use my HSA for?

Great. I can shelter some pre-tax money for healthcare costs. Given that this is one of the most expensive costs in retirement, it might be useful to know what you can use your HSA for, right?

The list is quite extensive, and the IRS publications on HSA’s state that what qualifies for an HSA would qualify as a medical or dental expense, which can be found online via the Publication 502 from the IRS.

Here are some of the highlights of things that are covered (in alphabetical order):

- Chiropractic Fees

- Contact Lenses, Eye Exams, and Eyeglasses

- Dental Treatment (teeth cleaning, x-rays, braces, extractions, dentures, etc)

- Diagnostic devices (think glucose monitor for diabetic patients)

- Eye Surgery

- Fertility Treatments (e.g. In Vitro Fertilzation)

- Hearing Aids

- Laboratory Fees

- Lodging and Food for hospitalizations ($50 per night per person)

- Long Term Care Services

- Medical Conferences (specifically for chronic ailments that you have, and you must attend sessions majority of time)

- Medications (prescriptions)

- Nursing Services

- Special Education (learning disabilities, teaching braille, etc)

- Sterilization (vasectomy, tubal ligations, etc)

- Surgery

Great, that’s a pretty exhaustive list. Actually, there are even more on the IRS website. These are just the one’s I’ve cherry picked so that you don’t have to keep scrolling

What are some salient things that do not qualify for an HSA’s use? This includes things like many insurance premiums (particularly if paid for by someone else, or where you receive a credit). You also cannot use it for premiums on other products like life insurance, disability insurance, or increased premiums caused by adding your spouse or children.

HSA Contributions limits 2020?

Alright. So, you’ve gotten this far, which means you probably have a high deductible health plan (HDHP) and access to an HSA. How much can you contribute to your HSA each year, then?

The contribution limits for an HSA are pretty straight forward. For year 2020, according to the IRS:

- Individuals can contribute $3,600 per year.

- If your family is also covered under your HDHP, then you can contribute up to $7,100 per year.

That’s a decent amount of tax-advantaged space for something that you are almost certain to use in your lifetime given how much health care costs during retirement. In fact, many can expect to spend at least $5,000 to $10,000 each year in retirement.

HSA vs FSA (Are they the same)?

Whenever I discuss HSA’s, someone will inevitably come join the conversation and unintentionally say something about Flexible Spending Accounts (FSA’s). For example, they’ll say, “Well, all of that savings sounds great, but you cannot roll it over each year. Use it or lose it, right?!?“

This person is confusing an HSA and an FSA. A Flexible Spending Account is a certain amount of money that you can place to the side each year to be used on medical expenses. This sounds a lot like an HSA, but it is not.

You can qualify for an FSA without a High Deductible Health Plan. This is still pre-tax money, but unlike a HSA it cannot be invested and it also disappears at the end of each tax-year. So, unlike an HSA you cannot rollover that money to the following year and keep it until your retirement days. If you do not use FSA money each year, you lose it forever.

So, to clarify:

- Both HSA and FSA money is pre-tax.

- Any unused HSA money can be kept and rolled over each year until you use it. Unused FSA money goes away at the end of the year each year.

- HSA money can be invested, FSA money cannot.

- HSA accounts require a HDHP whereas FSA’s can be used even if you do not have a HDHP.

- You cannot have both an FSA and an HSA plan at the same time.

HSA versus Low Deductible Plans?

Everything we have discussed so far has made the HSA sound like an obvious choice. Why wouldn’t everyone have an HSA?

Well, the High Deductible Health Plan requirement isn’t ideal for everyone. Look at those numbers from above. For example, if you are a resident physician earning the median income for the country ($55-$60,000 per year) you likely cannot afford a deductible and out of pocket maximum of $13,500 per year if you have a family.

Now, that said, you can use the HSA money you saved ($7,000 per year for a family) to pay towards any costs you incur towards your deductible. That said, you cannot cover it all if something catastrophic happens to your family.

So, while the HSA plan is great if you are otherwise healthy and a high-income earner, you need to compare apples to apples which means comparing a low deductible health care plan’s cost to a HDHP with an HSA if you used the money.

Should I Use My HSA for a Big Expense?

So, this is the ultimate question that ties all of this together. It is also the most common question that I get for active HSA owners.

“Hey, Jimmy, I just got a LASIK procedure. Should I use my HSA now or save the receipts for later?”

This is a tough question, because using the HSA money now or saving it for later are both reasonable decisions.

See, you can actually save your receipts and recoup the cost through your HSA at any time point down the road. In other words, you can use the money now or let the money grow in an investment account and (hopefully) get 6-8% in the market with the plan to turn the receipt in later.

So, what should you do? Well, that depends on your personality. If you are forgetful like me, using the HSA immediately is a very reasonable thing to do. However, if you are a mindful person who has the cash flow to pay for the expense now, then save the receipt.

If you do decide to save the receipt to get reimbursed another day, I’d recommend that you save the receipt in a reasonable way. For example, you might place them in a fire proof box or take a picture of the receipt and store it electronically in a cloud or Google Drive.

Just make sure that you know how to get to it when the time comes to pull the trigger on using the HSA.

Take Home

Learning about HSA’s is definitely in the 20% of personal finance that you need to know to get 80% of the results. It’s a great savings plan that can help you find success. It allows you to pile away more tax-advantaged savings (that may never be taxed), often provides index fund investment options, and is provided by many employers.

However, the HSA plan does not come without risk. It does require a High Deductible Health Plan (HDHP) and for you to save your receipts in a secure location if you don’t plan on using the HSA now.

Do you use an HSA? Where do you save your receipts if you are a saver? If you spend your HSA as costs come up, what’s your rationale for doing that? Leave comments below.

Thanks for the informative post. A few notes of clarification: 1) After age 65, HSA funds can be used to pay for non-medical expenses but are subject to ordinary income tax, 2) HSA funds can be used to pay for Medicare Parts A, B, D and HMO insurance premiums, and 3) you CAN have an FSA and an HSA at the same time; you just can’t contribute to both at the same time (i.e., once you have a funded HSA, you don’t lose it because in the future you contribute to an FSA).

All great points, Jeannette.

Now that the ACA has raised my family deductible to over $13,500 we are no longer eligible to contribute to our HSA. Huge increase in deductible, huge increase in premium, and loss of tax break. What a horrible travesty of a law!

HSA is tricky in states like CA and NJ where the deduction is not recognized. Because it’s a federal program, companies will not send you tax forms every year, so you’ll be on the hook for keeping accurate track of your cost basis, dividends, cap gains, etc. for this reason, some people will place in TIPS/treasuries to bypass the state tax pains.

Looking forward to having this avenue available once I get out of the military. As our income rises, we need every avenue possible to get legal tax deductions to reduce our overall tax burden. I think an HSA should be a part of any high income earning household’s financial plan. Good reminders on the FSA vs HSA concept as well.

-Brent

http://www.TheScopeOfPractice.com

Question about HSA and FSA.

I have a HDHP with my practice and we contribute to the HSA associated with this plan. My wife, with a different employer has coverage also on a separate insurance plan, and we contribute to an FSA through that separate insurance carrier. Her insurance also gives us access to a dependent care account.

Any concerns with this arrangement from a legal perspective?

For the record, not a lawyer or tax expert…. But I don’t think you can get reimbursed for HSA expenses on your wife if she is also getting reimbursed through an FSA. That seems like tax evasion/fraud.

So, I’d use the FSA account first for anything that she needs. Next year, you might consider only doing the HSA, because you could use that to cover your wife’s expenses (if needed) even if she has a different health care plan.

The dependent care flex account is different. That is covering a different expense.

My family has both an HSA and dependent care FSA. Not an issue.