At the beginning of this site (November 2017), I wrote my first Physician Philosopher Manifesto. In it, I detailed our financial goals, including when our student loan debt would be paid off, when we would buy our next house, and the age by which I’d have met certain investment goals. How old will I be when I get to financial independence? Keep reading to find out.

Part of the purpose of this blog is to track my family’s journey to financial independence. This usually occurs through net worth updates, which are tracked from “time out” since training (6 months out, 9 months out, 12 months out, and 15 months out).

Today, I want to provide a quick update on the goals from my original manifesto, and outline exactly how I anticipate getting to our financial independence number over the next ten to twelve years.

Defining Financial Independence for Us

For those of you new to this financial independence game, your FI number is the number at which you no longer require earning a paycheck. This can be accomplished through saving a “nest egg” from which you draw down money each year. Or, it can be from passive income.

Personally, I intend to take a hybrid model for financial independence.

What this means is that I plan to save and invest enough money to cover a substantial portion of our desired annual salary while we also have some passive income coming in to help provide any remaining money we need above which we have not saved.

The FI number by which we could stop working would provide $100,000 annually assuming that all of our other debts are paid off by this point (i.e. no mortgage, car loans, student loans, college for the kids, etc). If we were simply saving to get to this number, we would need $2.5 million based on the 4% safe withdrawal rule.

I’d like to get closer to $3 to $4 million just to allow for some built in safety, and this was my originally stated “FI goal” anyway. However, based on our current lifestyle, we would be FI at $2.5 million.

Side hustles, which can serve as one of the best asset protectors, will hopefully provide passive income from books, inventions, real estate, and (hopefully) this blog. Any money from these endeavors will decrease that $100,000 annual salary we would be trying to achieve through our nest egg.

So, if we come up with a steady $50,000 in passive income annually, then our FI savings number would have declined to only $1.25 million. We will be able to get to that number pretty fast as I’ll outline below.

Progress Report

In my first manifesto, I outlined several goals. All of these were based on “time out” from training. Here are the ones worth mentioning right now:

- $100,000 in assets by one year out (actually completed this in less than 12 months)

- Positive Net Worth by two years out. We started at negative $208,000 and met this goal in less than 15 months. Our next net worth update comes out at the end of January.

- Student Loans paid off by two years out (July 1st, 2019). We are on track to have our $200,000 in loans paid off by March 2019. We have averaged $10,000 per month in payments.

- Not buy a house until the loans are paid off. Oops! First payment will be due by January 1st, 2019. However, we will likely pay them off at the end of the same month.

- Millionaire by 8 years out from training. Not quite to this one yet!

As you can see, we are meeting all of our goals and more. We have made some changes along the way – like buying the house earlier than anticipated – but we have not sacrificed any of our progress.

Our Current Situation

To recap, we want to get to $2.5 million to reach our FI number and to $3.5 or so for comfort well above that (where we can draw down 3% and still have at least $100,000).

How do we plan to do that?

Well, here’s how it is going to shakeout. Currently, we have well over $150,000 in assets in our investment accounts.

For the past 18 months our planned monthly student loan payment has been $5,500 per month – which does not include our additional bonus pay that we put towards our loans.

Therefore, once our loans are paid off we will be able to cash-flow that number. Where will it all be going? Well, our new mortgage costs $2,000 more than our old one. So, $2,000 will be going to that.

After that, we are left with $3,500 to use every month towards our goals. $2,000 of this will go towards a taxable account each month, and $1,000 will go towards filling up our backdoor Roth IRA for the year.

The other $500 will be for enjoyment, per the 10% rule – which has been the key to our success.

(For the record, we only put $4,000 into our backdoor Roth IRA this year and used additional money to pay off loans, instead. Blasphemy, you say! It’s all about defining your goals – and our major goal was to be out from under our student loans ASAP.)

How old will I be when I get to financial independence?

Given our additional intended savings outlined above, this is what our annual savings will look like going into the separate vehicles:

- $45,000 into my 403B, which includes employer contributions/matching.

- $19,000 into my wife’s 401K

- $15,000 into my wife’s governmental 457 plan.

- $12,000 into the Backdoor Roth IRA

- $24,000 into a taxable investing account

This gives us an annual savings of $115,000, or a savings rate of 32% of our base salary.

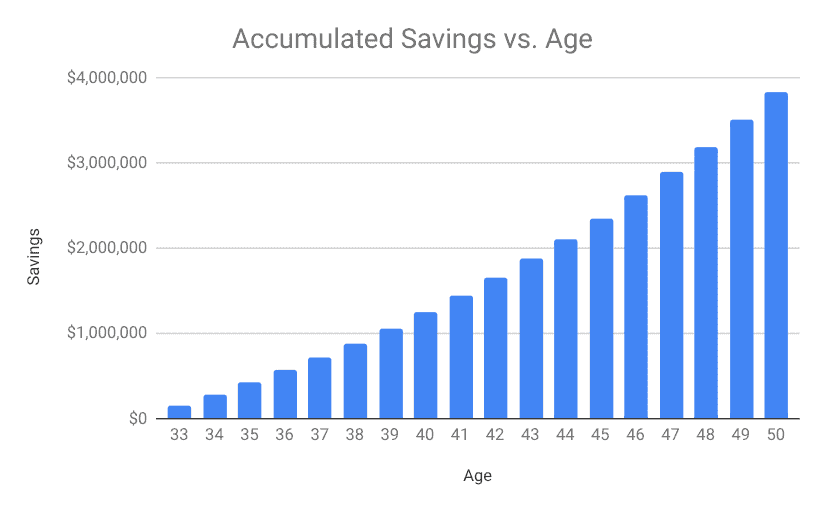

So, taking our starting $150,000 in assets and combining that with our intended annual $115,000 baseline savings – how quickly will we get to $2.5 million and $3.5 million?

Assuming 6% annual earnings, this is how it shakes out:

How old will I be when I get to financial independence? By the graph above, we should get to $2.5 million by age 46 and to $3.5 million by age 49. And this doesn’t include any 529 contributions.

If we received an annual return of 8%, we would get to each of these milestones about two years sooner (44 and 47, respectively).

We can do better!

The scary thing is that this is only our baseline savings rate from our base salaries. If we decided to, could we speed up this timeline? Absolutely.

The above chart doesn’t take into consideration any of my quarterly or annual bonuses. It doesn’t take into account the two car loans we have, which we will cash-flow once they are gone. It doesn’t take into account the $1,800 in childcare costs that we pay each month that will also vanish soon.

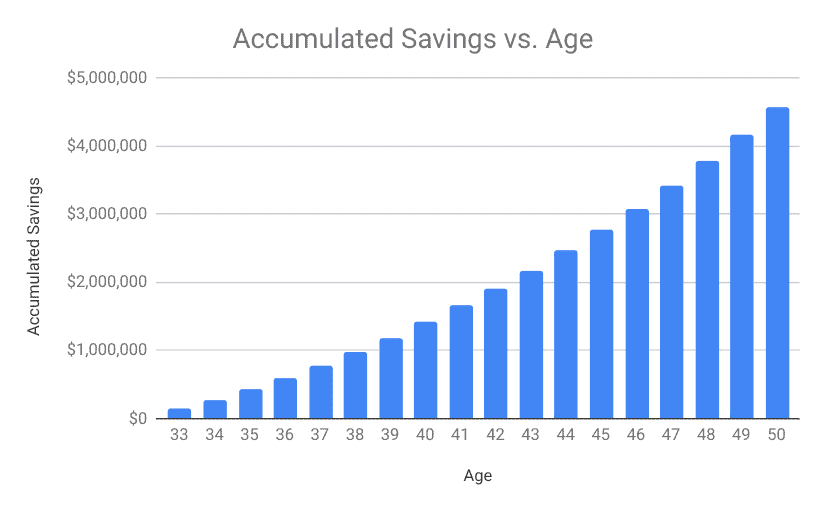

So, taking the above into consideration, let’s look at the accelerated plan. Here are the assumptions:

- We save an additional $750 per month next year when our little boy starts kindergarten.

- An additional $750 is saved when our youngest starts kindergarten.

- When the cars are paid off, we will save an additional $1,000 per month.

Still assuming a 6% annual earnings average each year, here is how it would shake out.

So, we would accelerate our timeline to achieve FI by age 44, and to reach an overabundance FI ($3.5 million) by age 47. If we actually receive 8% (instead of the 6% assumed above) we will shave a year and get there by age 43 and 46, respectively.

Still, none of that assumes a promotion, annual and quarterly bonuses, or any money made from side ventures like books, blogs, or inventions – all of which I anticipate will produce more income. (Note: 25% of this blog’s profit goes to charitable causes).

If we saved $10,000 more each year from my bonuses, we would be financially independent by age 42 and have $3.5 million by age 45. Again, this still doesn’t account for any side income.

Isn’t it awesome what you can accomplish when you set your mind to something!

Take Home

The above information is shared for two reasons.

The first is that I want to outline how we intend to get to our goals. I hope this serves as an example for those coming behind me. You can do all of this is you don’t inflate your lifestyle too quickly!

The second reason is that I’ll use this post to check back on our progress. This will hold my family and me accountable for what our stated goals were when we started.

The great thing about all of this is that these are OUR goals. Yours might look very different. Our goals, as stated above, also still allow us some flexibility to give money to those in need and to allow our family to take trips and vacations.

Remember, more money will not make you happier. But financial security does provide freedom and options to design the life you want to live.

What do you think about the stated goals outlined above? How does this look different from your own goals? Leave some comment love below.

TPP

It sounds like you are on a great path. I felt pretty rich when I made it to a positive NW of 500K. Then I hoped to be a millionaire one day. I reached it and realized it will produce 30-40K per year if I’m lucky. Shot for 2M then 2.5M. Currently, I tell most doctors to shoot for the 3-5M range.

Even though my wife and I are frugal, our spending has increased every year for 20 years. I don’t share this to discourage you. Just to highlight that we tend to move the goalposts when we get closer. That isn’t all bad. It keeps us coming up with new goals and areas of growth. Rock on.

That’s a good point, WD. I presume we will have the same experience and getting to that larger number will allow for some of that. I also want to be able to still give generously to people, and having more would make that easier.

Thanks for the thoughtful comment!

Congratulations on the predicted trajectory TPP. Your post actually made me feel good because at 47 I actually achieved your accelerated 6% rate of return goal which is remarkable for me because I had a massive hit to my net worth (via my well documented divorce) at age 39.

If that graph continues to work out for me, I might actually adjust my planned early retirement (53) a few years earlier (although I really think part time is the best option for me as I want to keep health benefits).

Part time with health benefits is a huge plus. And I actually really enjoy my work most days. So, I’ll probably follow a similar path unless things change

Very encouraging! I took out a piece of paper and chronicled my journey. I am somewhat late to the game but so glad I found WCI right out of residency, in my first attending job when having so much debt was uncomfortable. Thank you for sharing becuase this offers encouragement to many of us who are working hard.

Thanks for taking the time to comment, Janice. I appreciate the kind words. I am just trying to be a part of the solution.