[This post may contain affiliate links, which further the charitable mission of this website. You may read my disclosure to find out more details]

The new Tax Cuts and Jobs Act took effect in my February paycheck. The increase was substantial. I had previously made the calculations to determine how much it ought to increase my paycheck, but was eager to see what the number would actually be. Today we will answer the following question, “how does the tax bill affect me?”

[Make note that all of these tax changes will vanish in 2025 unless congress does something to keep them in place. That said, this is not a political post. So, take that for what it is.]

The Basics

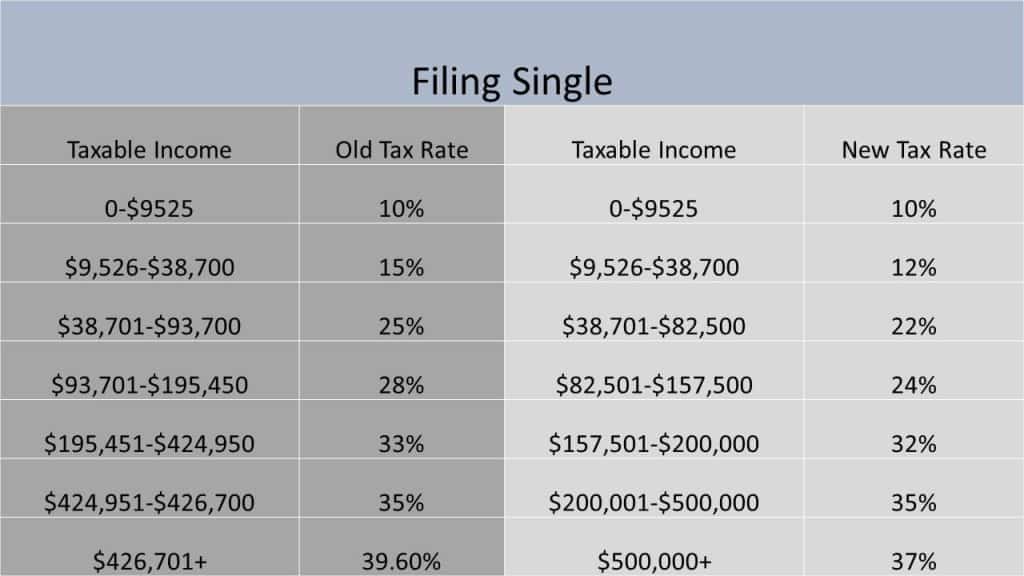

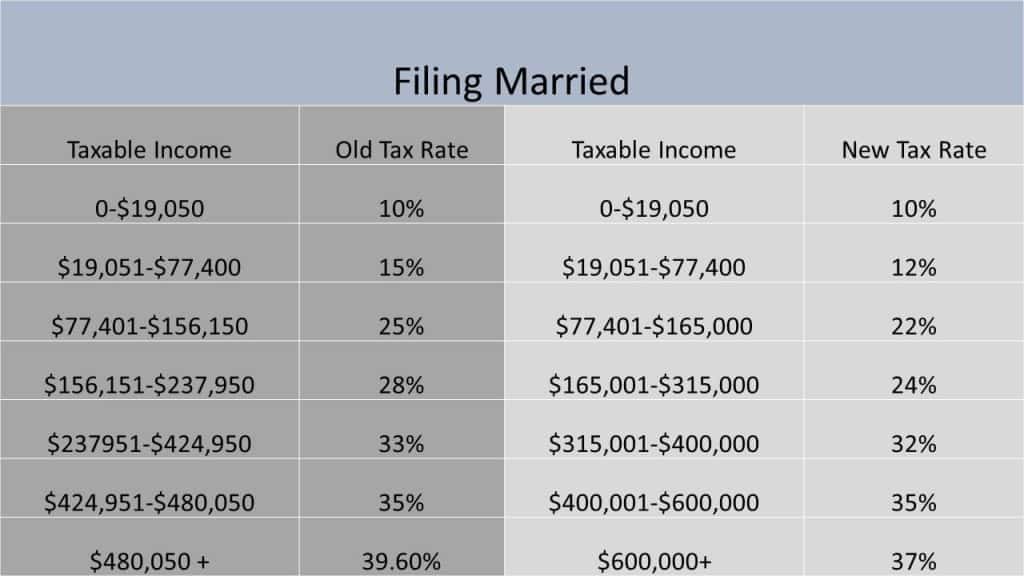

As many of you are well aware, there were many changes that took place. I want to discuss some of the basic changes that impact high-income earners. Below you can see the new bracket next to the old brackets for those filing married (jointly) and single. This, of course, is the federal tax system. The numbers below do not account for your individual state tax.

First some basics. Our tax system is a progressive tax system. That means that for increased bracket you earn you are subject to a new tax rate. For example, the first $9525 you earn as a single person in this country is taxed at 10%. So, once you have filled up this bracket with money you have paid $952.50 in tax. If your adjusted gross income increases even a dollar more than that first bracket, you begin to pay the next tax bracket for money made over that at the next tax rate (12% in this case).

The reason this is progressive is that your first $9525 is still only taxed at 10%. The money you earn above that amount (from the $9,526 to $38,700) is taxed at 12%. And so on.

Filing Single

For those filing single, here are some examples of income and how much is saved based on the new tax plan.

- If your adjusted gross income is $100,000 compared to the old tax plan, you can expect to save $2553.15 from the new system. That turns out to increase your monthly paycheck by a little more than $210.

- If your adjusted gross income is $200,000, you will save $3380.64. Monthly paychecks should increase just over $280.

- The numbers for $300,000 AGI are more impressive. In the old system you would have owed $82,079. In the new tax system you owe, $67,088. This makes for a difference of just under $15,000. You can expect monthly increases in your paycheck as much as $1250.

Well that’s great. What about those who are married filing jointly?

Filing Married Jointly

Of course, similar results can be found for those filing jointly/married.

Looking at the same examples as above, here are the numbers for those filing jointly and how much they save with the new tax plan compared to the old.

- $100,000 AGI. That couple saves $2428 annually, which comes out to a monthly paycheck increase of just over $200.

- For the couple earning $200,000 the annual increase is just over $6000. This equates to a monthly increase of over $500.

- Those earning $300,000. Annual increase in pay is north of $13,000. You can expect a monthly increase of about $1100.

Other impacts

While the above is a pretty nice increase for many of us who are earning high incomes, it doesn’t end there. The new tax bill also made drastic changes to the AMT, or the Alternative Minimum Tax. I’ve written about the AMT before, but the effect of the AMT on high-income earners should also be profound.

See, the way the system works is that you get taxed under both systems (the brackets above and the AMT). Whichever number is higher is the tax you pay. That hasn’t changed. For many people, the old brackets weren’t too bad. What was bad was getting hit with a higher tax through the AMT after that.

The changes are beneficial for most every physician and physician couple. In essence, as long as you are single and earn less than $500,000 or married and earn less than $1,000,000, then you most likely get to utilize the exemption in the AMT. Prior to the new tax law, many of us would get hit by the AMT and we would not be able take advantage of the exemption to decrease the amount we owed. We were getting hammered by an archaic law.

A Case Study on the AMT changes

For simplicity’s sake, and just to drive home the point, I’ll give the following example. Let’s say you are married, and make $350,000. In the old AMT system, this would have cost you roughly $94,260 in taxes. This would have been higher than the taxes you’d pay through the traditional bracket system. With today’s changes, the AMT would now cost you only $63,628. This is because you get to deduct the exemption ($109,400 for married; $70,300 for singles) from the AMT system before taxes are applied. This is because most high-income earners did not used to qualify for the exemption in the past.

This difference for a married couple who would have paid the AMT last year and who won’t this year could be substantial. Even in the new tax bracket system that couple with an AGI of $350,000 will expect to pay $75,378 in federal taxes. If you subtract the prior AMT they were paying above ($94,260) from their new tax payment ($75,378), this couple is now saving almost $19,000. That’s a monthly increase in their paycheck of about $1575.

That’s a lot of money.

So, how did this impact my paycheck?

Also, for any of the medical people reading this post… you should read this book. It’s good stuff.

I’ve published information on my annual base income before (~$300,000). This led to my monthly paycheck increasing about $1000. So, where did this money go? Well, I increased my monthly payments towards my student loans by $1000. I am now paying $5,000 in monthly payments each month instead of the $4,000 it was before. This is going to shorten my payback by about 4 to 5 months. I am still on pace to pay off all of my $185,000 in loans two years after finishing training.

One more note:

For the residents/fellows out there, the increase above is in addition to a pretty cool phenomenon I first experienced last year when I made my first attending paychecks for a few months : the social security limit. When I hit the social security limit of $127,000 my monthly paycheck increased another $1000-$1500.

For those of you that don’t know how the social security limit works, this is the number at which you stop paying medicare, medicaid, and social security tax. Up to $127,000 you are paying a 6.8% employee tax on your monthly paycheck to pay for these social programs (that may or may not exist when you get there, though that’s another topic for a different day).

So, after you have been paid more than the $127,000 you no longer have to pay that 6.8% tax. As an example, a person making $20,000 gross per month in their paycheck can expect to receive an extra $1,360 post tax. I love when this happens because I get to use that money to destroy my debt or aggressively invest even further.

How did the tax law impact your take home pay? Was it noticeable? Or did you barely even notice? Leave a comment below.

TPP

The tables above do not account for the standard deduction. For married filing jointly, that is $24,000. So, for instance, where the table shows a tax rate of 10% on $0-$19,050, that is in reality a 10% tax on $24,001 to $43,050, with 0% on $0-$24,000. So a couple earning $43,050 will pay only $1904 in tax, which is only 4.4%, and likely much, much less if they have anything else in their favor (like children).

Also, the FICA cap does not apply to the Medicare portion of the payroll tax, which continues on up for high income persons. No cap. 2.9% if self employed.