This is a guest post written by Dr. John Lim who is a well-known author in the personal finance world. He often writes for the Humble Dollar and has submitted guest posts to multiple WCI Network partners. Dr. Lim is in the process of creating a personal finance curriculum for his residents in Reno, NV. As you’ll see below, I’m sure that he will find great success in helping improve physician financial literacy!

If you do not know how to figure out your savings rate, this post may prove helpful. It has some math, but this is necessary when the rubber meets the road. Tag along as Dr. Lim discusses how to make residents care about personal finance, teaches his view on determining your spending and savings rate, and outlines his methods for his Spend Save Ratio process.

The Spend Save Ratio: How to Determine Your Savings Rate

Two major obstacles must be overcome before people can begin to get their personal finances in order. First, they must become financially literate. While this is no mean feat, it may actually be the easier of the two hurdles. I have long argued that learning the basics of personal finance and investing requires a relatively small investment in time and effort. It exemplifies the Pareto principle by which one can reap large financial benefits by mastering a relatively small set of financial principles. It is unfortunate and indeed ironic that financial illiteracy is so rampant in the current information age. Still, I am cautiously optimistic that progress will be made on this first front.

However, the second obstacle poses a far bigger challenge, one which I think deserves greater attention. The challenge is to change financial behavior. It is a leap of faith to assume that spreading financial literacy will necessarily lead to changes in financial behavior. The best analogy for this is the obesity epidemic. The rise in obesity is not for lack of knowledge on how to counteract it. Everyone knows that losing weight requires a reduction in caloric intake and increasing the amount you exercise. However, there is a huge difference between knowing and doing.

Do Personal Finance Facts Lead to Change?

Teaching people about the virtues of compound interest and saving for their retirement is important. But I am skeptical that head knowledge is enough to change financial behavior and habits.

In fact, sometimes modifying financial behavior has nothing to do with imparting knowledge.

For example, simply by auto-enrolling employees in their company’s 401k plan and having them contribute to it as the default, you can dramatically increase 401k participation rates (employees can always opt out of the plan or stop contributing, but few do so). This illustrates one of the greatest challenges in getting people to make better financial decisions, namely inertia.

Furthermore, it is hard to get people excited about saving for their retirement. The benefits are often decades away, whereas the pain—reducing one’s spending now—is immediate and tangible. You could impress upon them the benefits of compound interest and saving until you are blue in the face, but until it “clicks” for them, you are unlikely to make much progress.

For lack of a better term, behavioral personal finance explores the challenges of making things “click” for people when it comes to their personal finances. It attempts to bridge the chasm between knowledge and action. In short, behavioral personal finance is far more interested in seeking ways to nudge people towards better financial habits than in simply making them financially literate.

Financial literacy may be the prerequisite to good financial decision-making, but for a large number of people there will always be a sizable gap between knowing and doing. It is that gap that behavioral personal finance grapples with.

Behavioral personal finance is far more interested in seeking ways to nudge people towards better financial habits than in simply making them financially literate.

For me, these challenges are more than theoretical.

BUDGETING AND THE SPEND-SAVE RATIO

I am currently preparing a talk for the residents on budgeting. In my opinion, most budgets are far too complicated, which is why they mostly fail. A well-designed budget essentially accomplishes two things. The first is to enable one to save a good fraction of one’s income. The second is to avoid going into debt, i.e. going “over budget.” My 4-step budget is designed to be as simple as possible while still achieving these two goals. Here are the four steps:

- Determine your annual gross income (AGI)

- Decide on your annual savings (AS). (It should be no less than 20% of your AGI.)

- Make a list of your annual non-discretionary spending (ANDS). These are “needs” not wants.

- Use the budget equation to determine your annual spending allowance (ASA). This is your discretionary allowance or “wants.”

Budget equation: ASA = AGI – AS – ANDS

Notice that the only step that takes more than a minute to complete is step 3.

The heart of the budget is the principle of “paying yourself first”, which is step 2. The 20% savings rate is just the floor or minimum. Now, I could extol the virtues of a high savings rate until I am blue in the face, but would residents really be motivated to follow the advice? I needed buy-in.

Aha, behavioral personal finance to the rescue!

I suspect most residents couldn’t give a hoot about budgeting or savings rates. But address the burn-out epidemic among physicians and you have their attention. Heck, many of them are suffering from burn-out right now. [TPP: I couldn’t agree more. A good teacher doesn’t teach facts. They can use Google for facts. A good teacher makes people care about the topic, shows the importance, and then serves as a “guide on the side” in the face of a challenge. Our residents are burned out, and money plays a huge part.]

As the average medical school graduate carries a debt load of $200,000 on his or her back, this should not surprise us. My audience is mostly residents that are in their late twenties. They face a career that could easily span another 35 years or so. How in the world could I tie the 4-step budget to the predicament of physician burnout, thereby making it relevant to them?

The Spend Save Ratio (SSR)

The answer: the spend-save ratio (SSR),

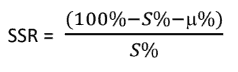

Spend-save ratio = spending rate savings rate

= (100% – savings rate) savings rate

Since every dollar is either spent or saved, your spending rate plus your savings rate equals 100%. For example, if your savings rate is 20%, then your spending rate is 80% and your spend-save ratio would be 80%/20% or 4.

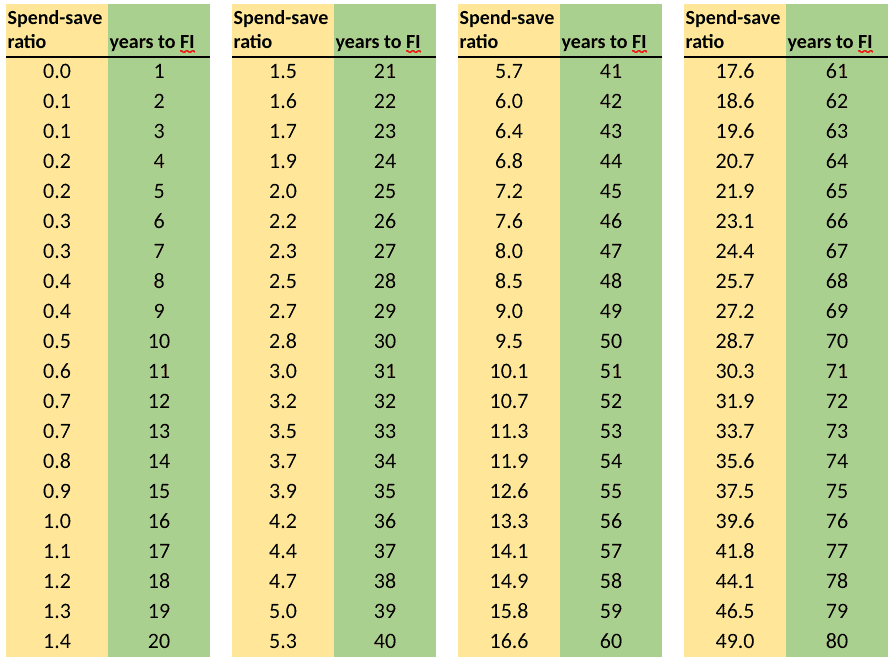

It turns out that this number, your SSR, is of critical importance to your financial future. I would argue that no number is more important. It literally determines when you can retire or reach financial independence (FI). In table A shown below, each SSR has a corresponding “years to FI” number. The lower your SSR, the smaller your “years to FI” number and vice-versa.

Table A

Before we do a deeper dive into the SSR and the assumptions underlying it, let’s review somenumbers based off of the SSR.

Let us ponder what these numbers imply for a 30-year old attending physician just starting out. A savings rate of 7%—about the average U.S. savings rate in the past decade—means a retirement age of 86! A 10% savings rate brings that number down to 79. And this does not even factor in any student debt. Pretty depressing.

What about the minimum 20% savings rate that I recommend? That allows for a retirement at the age of 65. This is actually very close to the average retirement age for physicians, which is reportedly 66 (versus 63 for the average American).

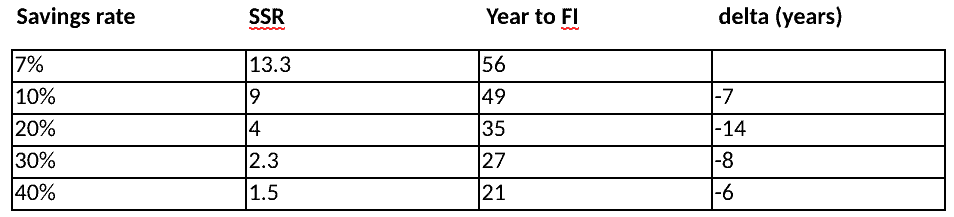

Now take a look at the last column, labeled “delta.” This is the reduction in years to FI by going from one row to the next lower row.

For example, by increasing your savings rate from 7% to 10%, you reduce your years to FI by 7. By increasing your savings rate from 10% to 20%, your years to FI fall by 14. However, note how the reduction in years to FI (delta) starts out rather high and begins to taper off. In other words, for each 10% bump up in savings rate, you begin to see diminishing returns when it comes to a reduction in years to FI. So, by raising your savings rate from 40% to 50%, you “only” shave off 6 years in your years to FI.

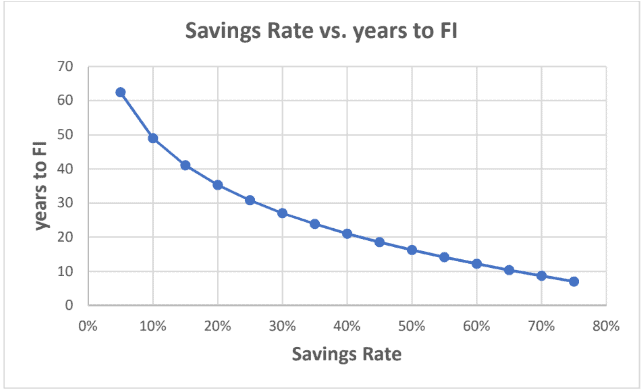

The following graph demonstrates this effect. Notice how the slope of the graph starts out rather steep on the left, but starts to flatten out to the right of the 25% savings rate point.

How Does New Spending Impact Your Savings Rate?

The SSR model assumes that what you have been spending during your career is what you will continue to spend in retirement. If you significantly cut your spending, you could naturally retire sooner. This is certainly a limitation of the model, but realize that downsizing your lifestyle is neither easy nor enjoyable, regardless of your age. This assumption also makes the numbers more conservative, which is prudent when planning for your retirement or financial independence.

However, one major spending item that disappears for many retirees is paying a mortgage. Fortunately, there is a simple way to adjust for this. Simply calculate your mortgage spend ratio, which is your total annual mortgage payments (principle and interest) divided by your annual gross income. If your mortgage payment is $3,000 a month and your annual gross income is $200,000, your mortgage spend ratio is (12 x $3,000)/$200,000 or 18%. Then, you would adjust your SSR calculation in the following manner, where S is your savings rate and is an adjustment factor, in this case 18%:

What about social security? Or pensions in retirement?

Both of these can be factored into the SSR using the adjustment factor. Let us say your total annual income in retirement from social security and any pension is “I” and your current annual mortgage payments are “M”.

Here are the complete equations for , the adjustment factor, and SSR:

A quick example. Let us assume you have an annual gross income of $220,000 and a savings rate of 20% (S = 20%). Your current mortgage payments are $36,000 a year. You expect a pension and social security benefit of $30,000 a year.

(adjustment factor) = ($36,000 + $30,000)/$220,000 = 0.3 = 30%

SSR = (100% – 20% – 30%)/30% = 50/30 = 1.67

Based on Table A, your years to FI is 22 to 23 years.

The Spend Save Rate Starts With Some Assumptions

A requirement or assumption of using the SSR model is that you begin with a net worth of zero. If you have a sizable net worth, this model does not apply. [TPP: What if your networth is REALLY negative when you start?]

However, the model’s original intent, hearkening back to behavioral personal finance, was to demonstrate to medical residents the direct link between their savings rate and years to FI or retirement. Since most residents have either a negative net worth due to student loans or a relatively negligible positive net worth, they can effectively use the SSR model once they have paid off their debts and have a net worth of zero.

For example, a new attending with student loansand a savings rate of 30% has an SSR of 2.3. This corresponds to 27 years to FI. If it takesher 3 years to pay off her student loans and reach “net worth zero,” the actual years to FI will simply be 27 + 3 or 30.

Another assumption that is made by the SSR model is that of a constant inflation-adjusted salary. Physician salaries are relatively stable compared to many other career paths. However, if your inflation-adjusted salary increases over your career, you will reach FI a little earlier than the SSR model would predict. Of course, if your salary declines, it will take you a bit longer to reach FI.

What About Investment Returns?

So far, we have not talked about the investment returns earned by one’s savings rate.

Clearly, if you have higher returns, your years to FI will be lower—all else being equal—than if you have lower investment returns. These assumptions are embedded in Table A. In the table shown, the assumed real rate of return was 5.4%. This is based on a 60/40 portfolio (60% stocks and 40% bonds) assuming historical real rates of return of 7% for stocks and 3% for bonds.

What if you have a very different asset allocation than 60/40? No problem.

Coming up with your own personalized SSR table using an Excel spreadsheet is a relatively simple matter. But here is the amazing thing. Changing your rate of return has a relatively small effect on your years to FI.

For example, if you assume a more aggressive 80/20 portfolio (80% stocks and 20% bonds), with a savings rate of 20%, your years to FI is 33 years—only two years less than for a 60/40 portfolio! This drives home the point that we should be spending much more time focusing on our savings rate rather than obsessing over our investment returns.

Parting Thoughts on Savings Rates

One’s savings rate is of utmost importance to one’s personal finances and financial future. However, knowledge of this does not guarantee a change in behavior, such as the adoption of a higher savings rate. I believe the spend-save ratio (SSR) is an extremely power tool in the arsenal of behavioral personal finance because it directly relates one’s savings rate to

the years to FI or retirement. The latter is something people really care about and is more likely to motivate changes in behavior. If I see that by raising my savings rate from 10% to 20%, I can reach financial independence 14 years earlier, that may be the necessary motivation to save more.

Moreover, if I employ a simple 4-step budget that prioritizes saving or “paying myself first,” and have those savings automated, I am much more likely to succeed in reaching my goal of a 20% savings rate. Such a budget is yet another behavioral nudge.

Finally, if I work together on budgeting with like-minded friends—financial accountability partners, so to speak—I am more likely to stay on track than if I tried to go it alone.

Behavioral personal finance is really a multi-pronged strategy. The SSR provides the crucial link between an abstruse “savings rate” and something I really care deeply about (years to FI). It provides the “Eureka!” moment. Automating my savings and similar budget strategies fight the inertia and limited will-power that inevitably afflicts us all. Having financial accountability partners or a social network to motivate us, keep us honest, and lift us up when we stumble is invaluable.

Is the SSR a precise planning tool? Probably not. But precision is rarely the determining factor in long-term financial success. If it helps you visualize the link between your savings rate and when you reach financial independence, and that insight motivates you to save more, than it has served its purpose. By bridging the gap between knowledge and action, the SSR exemplifies the power of behavioral personal finance.

TPP’s Thoughts on Savings Rate

TPP: My views on budgeting involve a little less math as I use a Backward’s Budget. However, it is built on similar principles. Pay yourself first. Automate your savings, student loan payments, and other financial goals. Then, spend what is left. Dr. Lim’s approach, though heavy in math, follow similar principles.

I’d love to hear more about how you budget, decide your savings rate, and determine big picture financial goals. Leave some comments below!

TPP,

Reducing caloric intake and increasing exercise is incorrect. And unfortunately this is what doctors are taught in med school along with bad nutrition advice which is then passed to their patients.

Doing the above is exactly what the competitors on the The Biggest Losers did and they have regained their weight and lowered their metabolic resting rates!

Exercise is benficial in that it will increase muscle mass, increases flexibility and strenght. But exercise is not for weight loss. This idea has been marketed to us.

In order to lose weight, you need to control insulin. You can exercise all you want but if Insulin is high, you will never access your stored fat to burn as energy. And Insulin will make you store more fat.

Weight loss is hormonal, it’s not a function of exercise or calorie reduction.

Dr. Jason Fung has an excellent explanation on this and so does Dr. Tim Noakes. You can’t outrun a bad diet.

So, this is a pretty nerdy article on financial planning, and I LOVE that! The spend-save ratio really puts some cold financial calculation on the whole process of thinking about how much you need to spend/save to reach your financial goals. I think it’s hugely valuable to see how you can shorten your time to FI by a decade or more just by increasing savings 5-10%. Great analysis!

-Brent

http://www.TheScopeOfPractice.com

Yeah, John really nailed this one. It is a lot of math, but the FI table was super cool!

Thank you for sharing this interesting article. I’m sure the difference to FI is larger with an increased savings rate when comparing a 80/20 vs 60/40 asset allocation. The question then becomes if one is saving greater than 30 or 40% if taking the additional risk of an 80/20 portfolio is worth it.

Thank you again for spurring folks on to becoming more financially literate 🙂