This is a guest post from David Graham, MD where he provides a case study – including visual representations – on the Trinity Study, safe withdrawal rate, and sequence of returns risk. It is a fantastic post that might really get your gears turning.

Dr. Graham is a practicing infectious disease physician who works as a flat, Fee-only financial advisor in his spare time. He passed the CFP exam, but doesn’t plan on pursuing the CFP marks. His goal is to help other physicians find financial independence, and he runs the site FI Physician. We have no financial relationship at this time. Take it away Dr. Graham!

What is a Safe Withdrawal Rate? A Case Study on The 4% Rule

Let’s get right to it. So much is written about the 4% rule that I assume you know the basics.

You have $1 million dollars and 30 years left to spend it. A Three Fund Portfolio sounds good, and you select a 60/40 stock/bond asset allocation. You have $400,000 in a brokerage account, $400,000 in a 401k, and a Roth IRA worth $100,000.

As for asset location:

- Brokerage: $100,000 in US Stock, $200,000 International Stock, $200,000 US bonds

- 401k: $200,000 in US Stock and $200,000 US Bonds

- Roth $100,000 in US Stock

The Safe Withdrawal Rate with a Moderate Portfolio

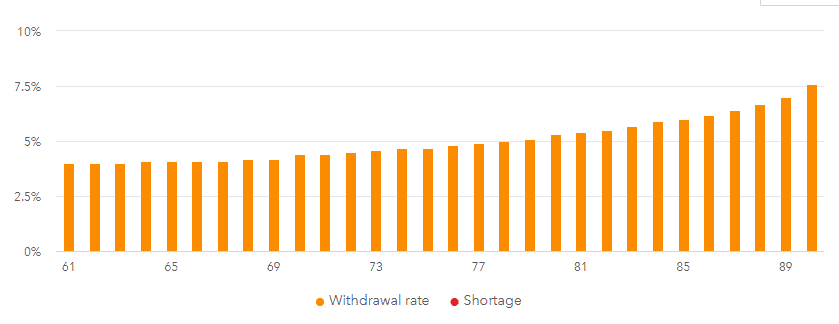

Figure 1 demonstrates the 4% withdrawal rate from a moderate 60/40 portfolio over time. You start taking $40,000 the first year, and increase that dollar amount by inflation each year. Since inflation is assumed to be 2% in this scenario, the second year you would take out $40,800, and so on.

Figure 1 (60/40 portfolio)

Note that although you start at 4%, because your portfolio has investment returns, the withdrawal percentage only very slowly goes up over time. The maximum withdrawal rate is about 7.5% of your portfolio a year at year 30.

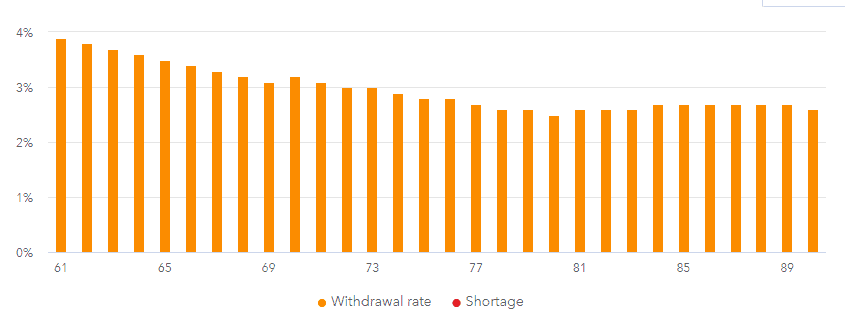

What if you changed your asset allocation to a much more aggressive 90/10 asset allocation?

The Safe Withdrawal Rate with an Aggressive Portfolio

In figure 2, note how the withdrawal percentage actually decreases overtime as your 90/10 portfolio earns more than you take out each year. This is despite of inflation and the 2% increase in the dollar amount you withdrawal every year. In order for the withdrawal percentage to decrease, you must be making more in your portfolio than you are taking out.

Figure 2 (90/10 portfolio)

How much does your portfolio grow each year? Well, to know that, you need a crystal ball.

Assumptions of Future Returns

Instead of a crystal ball, let’s assume that Vanguard’s recent assumptions hold true. They have released an Infographic and a PDF with the following assumptions for 10 year returns: US equities 4-6%, US bonds 2.5-4.5%, International equities 7.5-9.5%.

To keep things simple, for this example we will use 5%, 3.5%, and 8.5% returns, respectively.

Comparison of the 90/10 and 60/40 Portfolios

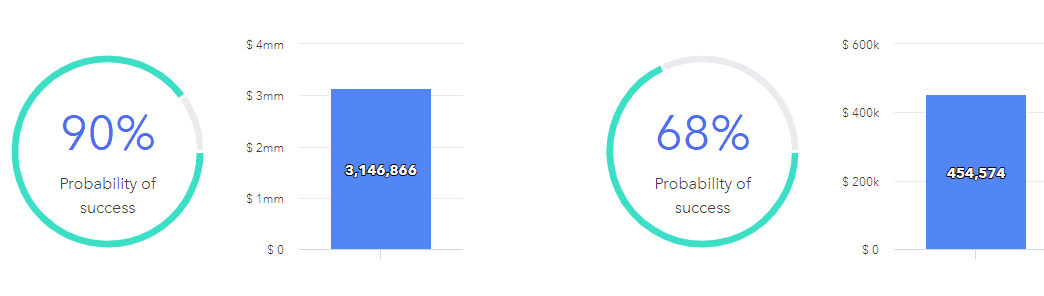

Figure 3 (90/10 and 60/40 portfolio comparison)

Above we see the Monte Carlo success percentages and final balances of the 90/10 (left) and 60/40 (right) portfolios. Note the chance of success given the return assumptions from above is 90% for the more aggressive portfolio compared to 68% for the balanced portfolio. There is a lot more money left after 30 years as well.

So why would you ever use a less aggressive portfolio? The answer to that question is Sequence of Return Risk.

Sequence of Return Risk

When you are drawing down on your portfolio, negative returns of the stock market cause you to reverse dollar cost average. This rapid initial depletion of your portfolio can cause long term failure after just a few negative years. Sequence of Return Risk (SORR) describes the failure of your portfolio determined by the returns before and after you start withdrawing from your portfolio.

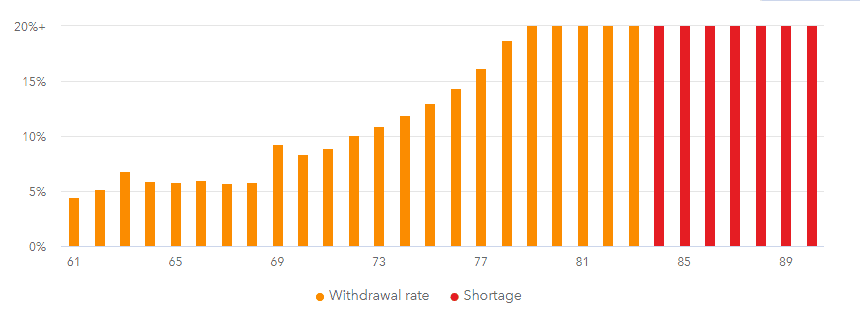

How does SORR affect a 90/10 portfolio?

SORR and an Aggressive Portfolio

Figure 4 (90/10 portfolio with SORR)

Figure 4 shows the same 90/10 portfolio we saw above, only we are using the actual returns from 2000-2010 instead of the assumed Vanguard returns. As you can see, the withdrawal percentage rapidly increases to unsustainable levels, and the portfolio runs out of money at age 84.

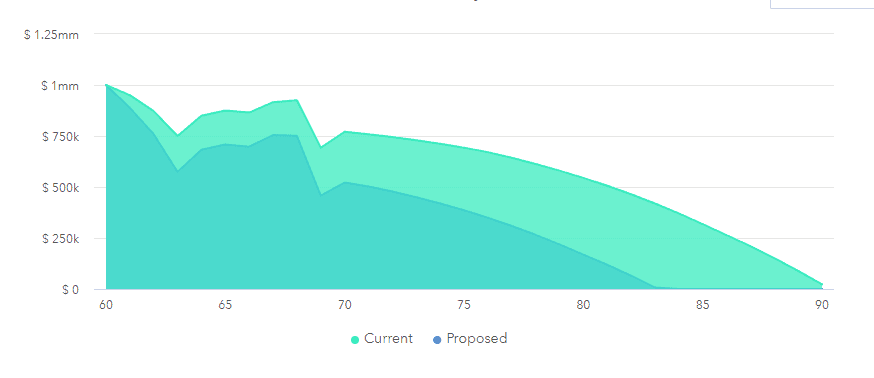

Let’s compare the drawdown of the 90/10 and the 60/40 portfolio using the actual returns from 2000-2010.

Drawdown Comparison

Figure 5 (Drawdown comparison with SORR)

Above, we can see the 90/10 portfolio in dark green and the 60/40 portfolio in light green. With the more aggressive portfolio we see large losses during the negative years which are not made up for during the positive years. The aggressive portfolio runs out, whereas the moderate portfolio just makes in to the end of the plan.

The 4% Rule Revisited

So, what is a retiree supposed to do?

If you plan on a 30 year retirement, the 4% rule is safe if you take SORR into account in your asset allocation. Use a moderate portfolio 5 years before to 10 years after your retire. Before and after these times when you are most susceptible to SORR, you can take more risk with an aggressive portfolio.

Some Parting Thoughts on the 4% Rule

The 4% rule is a hallmark of FIRE. This Safe Withdrawal Rate calculates your FI number: 25x your annual expenses. There are many good and bad blogs about the 4% rule, but I will leave you with the following thoughts:

- US historical returns are considerably better than other countries’ returns

- 30 years is the general limit of the 4% rule

- SWR ignores social security and other income sources

- William Bengen’s original research used a 50/50 portfolio with 5 year treasury bonds

- The Trinity Study compared different withdrawal rates to different stock/bond portfolios.

- The Trinity Study used higher volatility corporate bonds rather than treasury bonds

- 4% is only used the first year to get the withdrawal dollar amount

- Subsequent years, the dollar amount is increased by the Consumer Price Index (CPI)

So, when it is your time to retire, will you use the 4% rule? It’s probably a good place to start, but flexibility is the key. Investor, know what you control. Behavior is key to investing and to a safe withdrawal rate.

What do you think? Do you plan to follow the 25X rule to financial independence and withdrawal 4% in retirement? Does this post make you second guess your asset allocation? Leave a comment below.

Editor: Please, take some time and visit FIPhysician for more great posts like the one above.

Another great post David (I am getting spoiled by all your posts on all the blogging platforms, you are doing a media blitz and are quite prolific this month).

That is an interesting concept of going down to a less aggressive portfolio 5 years before retirement and during initial retirement phase and then going back into a more aggressive tilt after you bypass the SORR time frame. However say you did do this and survived the first few years of retirement and switched to a more aggressive portfolio, does the portfolio still survive if the SORR happened in years 5-10 of retirement? (I. E. You protected against a SORR that never happened, survived the danger time period and then feel confident to go more aggressive and bad timing hits you with a bad SORR then).

David’s posts have been on the money! Completely agree. And I think he even has a guest post coming out that will answer your question!

Thanks for the compliment XRV! It is a lot of fun to get featured on TPP’s site!

The short answer to your question is yes. The “rising equity glidepath” protects you in a 30 year retirement if SORR strikes at year 5 or 10.

For a 60 year retirement, well, I have a post on that exact topic expect out in a month or so.

Great post. This encourages me to keep our plan of saving more and will retire a bit older. Having more cash will make it easier to vary our spending.

These calculations always assume same spending year after year, but in realty that seems very unlikely. In real life, young retires seem more likely to spend more early, during the go-go years, and then less and less during slow go years, until maybe healthcare/assisted living kicks it back up in no go years. How do we plan for that?

I think flexibility in the early part of retirement is key. Being able to cut back if needed (or spend more if able) is essential to success.

I agree, that’s why I wonder if folks could try 5 or 6 % early on, and then adapt based on market, lifestyle, health etc. Especially if one has a little large account, more flexible. Might miss out on a lot of fun being too conservative, especially when younger and healthier

This is great. I’m 60/40 54 years old semi retired. When I start drawdown, could be any time but I’m thinking in about 5 years .

I’m UK based investor. I’m tending towards 3.5 % swr as I’m not over weight in US equities and have cash instead of bonds.

If 40% of your portfolio is in cash, I’d highly consider having it at least in a high yield account that keeps up with inflation. Otherwise you are losing money there each year in what should be the “fixed” portion of your allocation.

Hi . Yes I’ve got the cash part in various savings bonds, isa, some is in an index linked guilt, ns and I inflation linked bonds which they dont offer anymore, but when it matures I let it roll on again.I’d say im just about keeping up with inflation .just couldn’t decide on a bonds index funds tbh with the threat that intrest rates could rise and bond funds would loose money. I still keeping wondering about a bond fund.every now and again I look into it again. What do you use?

I have had several clients withdrawing 4 to 5% for over 20 years in every case they have at least their original principal

The last 20 years? Including the most unprecedented 10 year bull market we have ever seen?

Probably could have taken even more.

I think 4% is a very reasonable starting place. There are certainly situations where more can be taken, and that’s great!

Thanks for the post, David.

You need SORR because the (standard definition of the) safe withdrawal rate is blind to prevailing market conditions and there is no scope to adjust withdrawals in light of actual investment performance outcomes.

If you retire near the end of a bull run, your 4% withdrawal rate rises to 5, 6 or 7% depending how bad the ensuing slump is, so you risk running out of money before you die.

On the other hand, if you retire near the end of a bear run your withdrawal rate gradually falls below 4% as the market recovers. You run the risk of under-paying yourself and having a large pile of money left over at the end of your life (good news for your beneficiaries!).

Will your world fall apart if you don’t get your inflation-adjusted increase for a couple years? I suspect not.

I suggest a simpler approach: just pay yourself 4%. On each anniversary of your retirement, check the value of your pension pot, divide by 25 and that’s your income for the following year. Simple.

“But that means my income could go DOWN”- yes, it could, and we can look at ways to address that. The upside of this simple approach is that you will NEVER completely run out of money – that is a mathematical certainty.

So, to moderate the effect of negative investment returns on your withdrawals, I suggest that if your annual review (based on 4%) indicates a lower withdrawal amount than the previous year, calculate a withdrawal based on a higher percentage such as 6% and pay yourself the LOWER of last year’s income and the 6% amount you just calculated. This ensures that your income will only ever go down if your portfolio drops by more than 33.33%, which will hopefully be a fairly rare occurrence.

I tested this out for a Brit retiring early January 1990, invested 100% in a UK (FT All Share Index) tracker starting with £150,000 in his pension pot. First year’s income of £6,000 more than DOUBLED to £14,428 by 2002 before dropping to £11,960 the following year.

It then rose to £13,707 until the Credit Crunch forced it down slightly to £13,237 in 2009. After that it rose to £15,756 in 2020. Average annual increase over the first 15 years was 4.7% and over the last 15 years was 1.85%.

The value of the pension portfolio rose over the 30 years from £150,000 to £386,000.

I imagine returns from the S&P 500 would have been even better over this time.

I plan on keeping two years of withdrawals in a “cash preservation account that earns only about 1.5 percent. The rest of my portfolio is heavily invested in stocks. Looking back at the 2008 Great Recession, my portfolio recovered about 90 percent of it’s losses in one year. It took another year to get the remaining 10 percent. Perhaps the market could crash and not recover, but we will have more problems than a bad stock market if that happens.