As part of this website I plan to follow my success in increasing my net worth and gaining ground towards becoming financially independent. I want to be as transparent as I can to allow people to see how this can be done via a real person who is making real decisions (good and bad). The following is a look into my portfolio.

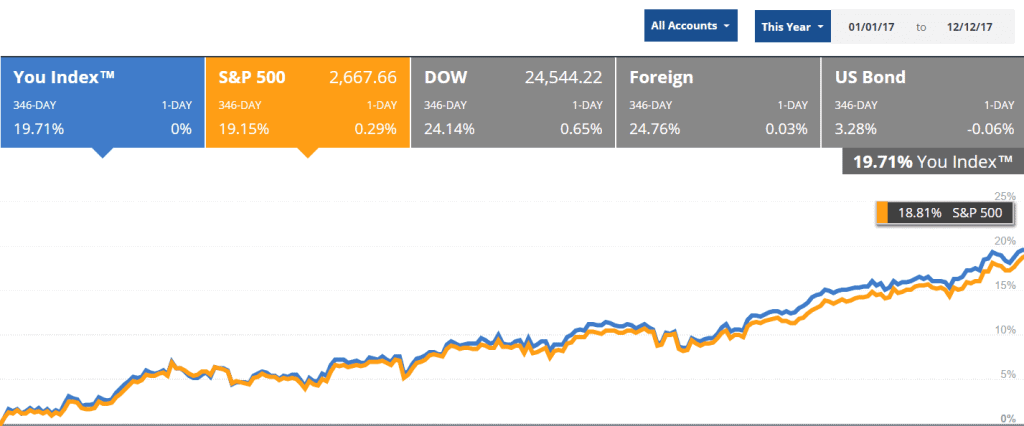

First, here are the results of my portfolio (up 19.71%) compared to the S&P 500 (up 19.15%) since January. This is captured on Personal Capital (good software for tracking/building wealth!):

Since 1/2017 how my portfolio has performed compared to S&P 500

For now, I have a very aggressive profile (100% stocks) because I am young and can handle the volatility. Adjustments will be made as time goes on! Here is how the TPP portfolio currently stands.

Current TPP Portfolio

Important to note: I am an academic anesthesiologist working at a 501(c) organization and my wife (Mrs. TPP) is a part time elementary school teacher that does not have access to all of the school system benefits as a part time worker.

TPP 403B:

Before we go into the breakdown noted below, I should state that my $18,000 this year (and $18,500 starting next year) goes in via the Roth mechanism. If you want to know more about my thoughts on this you can read my post on Roth versus Pretax contributions. There are a lot of different thoughts out there on this. My employer also matches/vests an additional $29,000 on top of this for an annual contribution of $47,000.

- 45% Large Cap Stocks

Unlike this frosty December day, my portfolio has a sunny outlook! Seasons change, though, and so will my portfolio as it is needed!

- Vanguard Institutional Index I Fund. Expense Ratio = 0.04%

- 20% Mid Cap Stocks

- Vanguard Mid Cap Index Admiral Fund. Expense Ratio 0.06%

- 20% Small Cap Stocks

- Vandguard Small Cap Index Admiral Fund. Expense Ratio 0.06%

- 15% International Stocks

- Vanguard Total International Stock Index Admiral Fund. Expense Ratio 0.11%

[Note: I later added bonds, and the allocation changed somewhat after that point. Additionally, I now – in my peak earning years – started investing pre-tax to pay down debt faster]

TPP Back Door Roth.

Currently, the TPP Backdoor Roth is the following:

100% Vanguard Total Stock Market Index Fund (Investor Share): $5500

*NOTE: The admiral share version of the Total Stock Market Fund has a much lower expense ratio, but requires $10,000. So, once I make my next Roth conversion, I’ll switch to the admiral shares version instead of the investors version.

TPP Taxable Account: Zero Dollars

After I fund my backdoor Roth money, this will be where my money goes next. This will come with paying down debt and advancement in my career.

TPP Employer 457: Zero dollars.

I do not anticipate investing in my employers non-governmental 457 at this time. I would also save this investment for the last thing after investing in other vehicles listed in this post (including Mrs. TPP’s investment vehicle).

Mrs. TPP 403B via School System

At this time, we do not have access to this account. Once our littlest is closer to elementary school, she will likely go back to full time work and we will contribute 18,500 per year into this.

Mrs. TPP 457 (Governmental) Plan – 100% stocks

Important Note: For those reading that do not know, there are substantial differences between governmental and non-governmental 457s. Same part of the tax code, but vastly different.

In our state, we do have access to this even though my wife is a part time teacher. We contribute (pre-tax) $18,000 per year ($18,500 starting in 2018) into this. This is pre-tax because we could not max out the Roth option given her lower income.

There are limited options. She does not have access to vanguard accounts here, and BlackRock is the next best (low cost) index fund. Here is the breakdown for this vehicle:

- 40% School Systtem Large Cap Index Fund. Expense Ratio 0.04%

- 40% School System Small/Mid Cap Index Fund. Expense Ratio 0.05%

- 20% School System International Index Fund. Expense Ratio 0.09%

Mrs. TPP Backdoor Roth

Currently, the Mrs. TPP Backdoor Roth is identical to mine:

100% Vanguard Total Stock Market Index Fund (Investor Share): $5500

*NOTE: The admiral share version of the Total Stock Market Fund has a much lower expense ratio, but requires $10,000. So, once I make my next Roth conversion, I’ll switch to the admiral shares version instead of the investors version.

Mrs. TPP Taxable Account

You may have noticed a trend here. This may happen once our debt is paid off.

Other potential investment vehicles in the future:

If this website continues to take off, someday I’ll likely open up a Solo401k. Given our 403B contributions above (which, unlike a 401k, are considered owned by you and not your employer), we will be able to invest an additional $35,000 into this account.

A solo401k is preferred over a SEP-IRA because it allows me to still participate in a backdoor Roth without having to worry about the pro rata rule.

What do you think? Was your portfolio similar to mine at this point in your career? Or do you plan on having a similar portfolio when you get here? Too aggressive? Not aggressive enough? Leave a comment.

TPP

[Edited on 1/20/18 because of some math at the end of 2017 that led me to make some changes]

In my day at your stage I was investing my entire 1099 amount into the market. After I got out of the Navy I started doing locums gigs living off the per diem. We had no kids and no debt. I took longer contracts (3-6 mos) made the hospital get me a condo. There weren’t anything like the potpourri of retirement accounts available then. We had IRA’s and the max contribution was $2000. We had SEP’s which maxed at about $22K. 401K’s were around but through an employer. Vanguard had only been in business for 10 or 15 years and was tiny compared to today’s standards. Index investing was nowhere on the horizon. To buy a stock cost about $200 through a broker. No Roth No ETF’s. The early 90’s were a bit of a bear market. It was a time of stock picking, fund picking, fund manager picking high fees and loads. Money went into funds like Fidelity Magellan and Fidelity Contrafund. It was hard to invest in those days because of the cost structure and tax consequence, none the less it was really the only game in town. There was no internet, no linked accounts and transactions were by mail. There were a lot of tax shelters.

Today investing is cheap and virtually effortless. Multiple tax deferred vehicles, really favorable tax law. It’s a golden age of ownership.

Sounds like it was tough back then!!! Much more intuitive investing now, but only if you put a little effort in to learn the ropes. I still have a brother in law who (despite many episodes of good advice) invests in cryptocurrency and pretty much nothing else.

Sometimes we are our own worst enemy even when their are now good options out there available to us!

One word: diversify

I believe Personal Capital reports the S&P 500 without dividends being reinvested, so your You Index looks better in comparison than it might really be. I think this is a marketing technique by them, and a bit dishonest.

Do you do any tracking of returns and asset allocation in excel? I’m kind of a junky for it.

What’s your goal/target? Are you on track?

I always enjoy when people share their data, and I think you could expand on this post to show your progress towards some end point. Drop me a note if you want to collaborate on something like that.

P.S. Awesome job on the expense ratios 🙂

I don’t have a specific goal, though I’d love to average anywhere between 6-8%. I think that’s pretty reasonable. You can see from my portfolio selection that I am an index fund kind of guy. So, I am just trying to diversify and trust that the market will do what it has done. I don’t aim to do any better or worse, and am okay with that.

For specifics asset allocation, you can check out my net worth posts. And this one too for the most recent one.

TPP